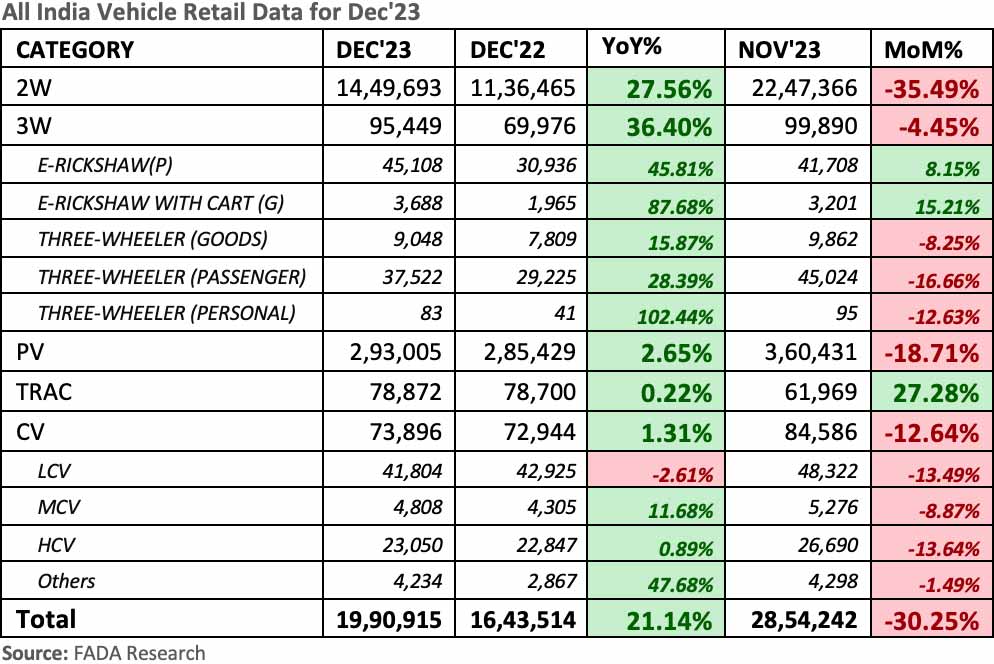

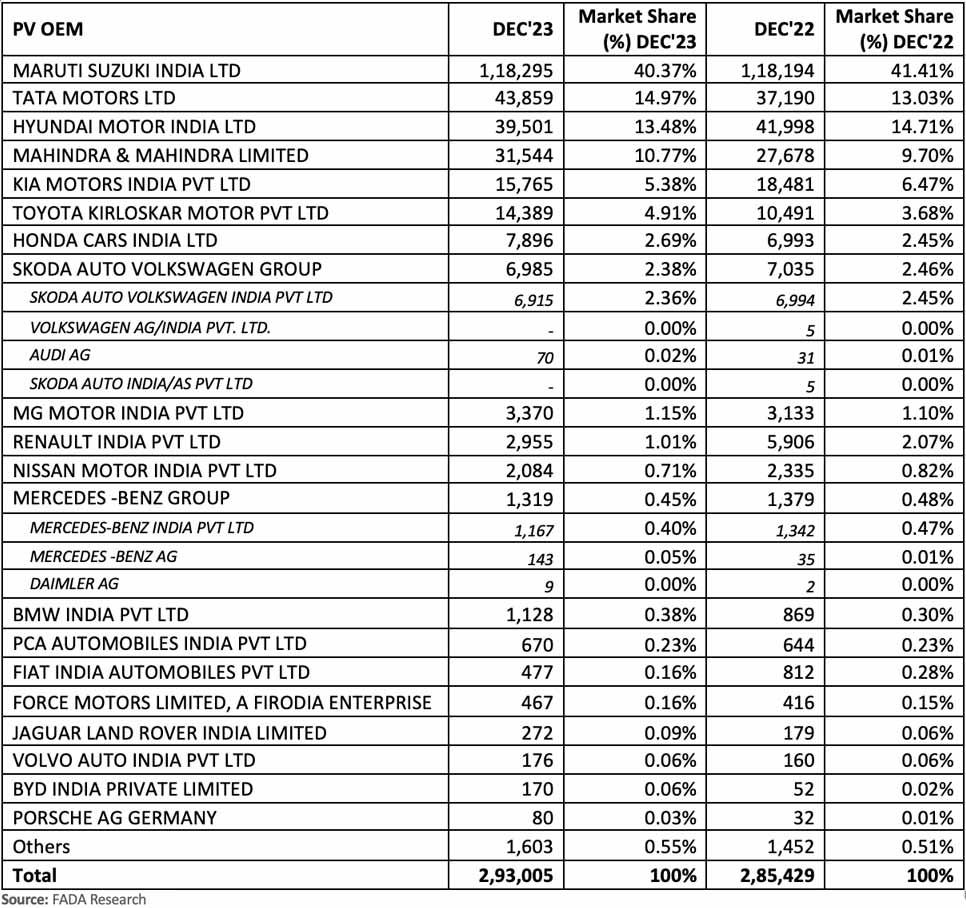

The Federation of Automobile Dealers Associations (FADA) has published December 2023 vehicle retail data, which shows an overall increase of over 21% compared with December 2022 data. The Passenger Vehicle (PV) segment, in particular, sold a total of 2,93,005 units last month, registering a YoY growth of just over 2.6%. Interestingly, Tata Motors pushed Hyundai to third place in the PV segment last month, while Mahindra continues to hold its fourth place by retailing 15,700+ more vehicles than Kia.

Notice that all segments and sub-segments were in green last month except for the LCV. The two-wheeler segment with a growth of over 27.5% was pretty impressive, and the three-wheeler segment with a growth of 36.40% was not bad either. The three-wheeler (personal) sub-segment registered an impressive triple-digit growth in Dec 2023. The tractor segment registered a marginal growth of 0.22%, but still, not bad at all. FADA President Manish Raj Singhania had the following to say:

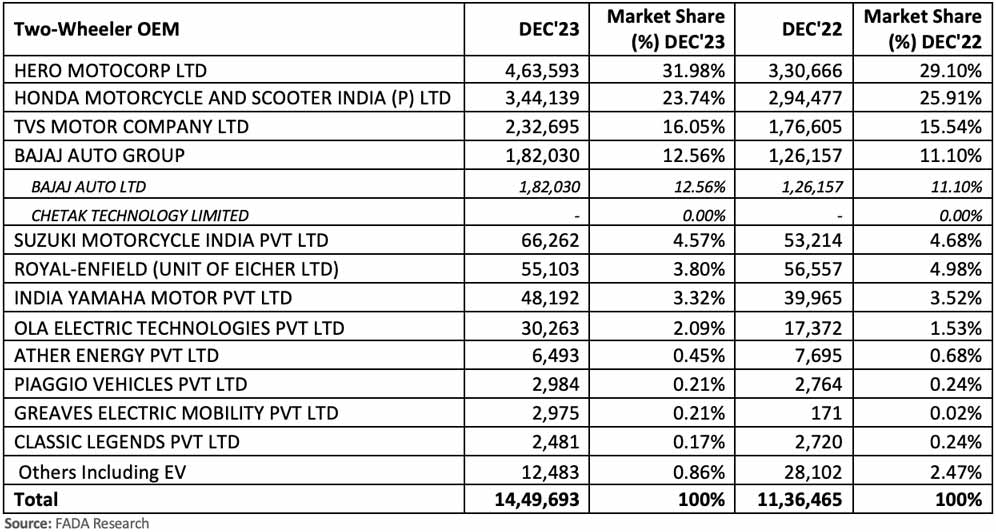

In the 2W category, key drivers included an abundance of marriage dates and the distribution of harvest payments to farmers, which enhanced purchasing power. Additionally, the availability of a wide range of models and variants, coupled with favorable weather conditions and a generally positive market sentiment, contributed to this robust growth. Enhanced product acceptance, particularly among the youth, and lucrative financial options, coupled with the anticipation of price increases in January 2024, spurred purchases.

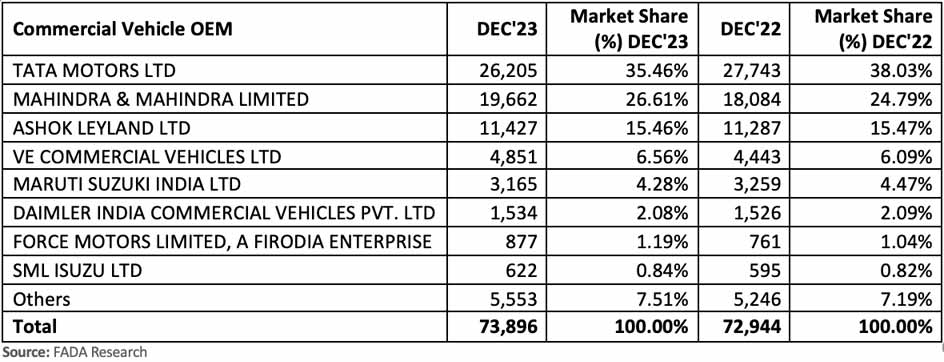

The CV category experienced positive growth as increased industrial activity and infrastructure development continued to fuel demand for M & HCVs. The bus segment also saw a rise, particularly in tourism and transportation, aided by orders from various state transport departments. Additionally, robust liquidity in rural areas and the financial boost from crop sales supported customer purchases, although retail cases remained somewhat subdued despite some pre-buying in bulk.

In the PV category, SUVs in particular saw strong demand, with extended waiting periods for key models. This surge was fuelled by aggressive year-end promotions and the introduction of new models. However, a significant concern was the high inventory levels, reflecting over-supply. This ongoing issue of high PV inventory, despite a slight decrease by the year’s end, remains a critical area for OEMs to address, emphasizing the need for further moderation in inventory management.

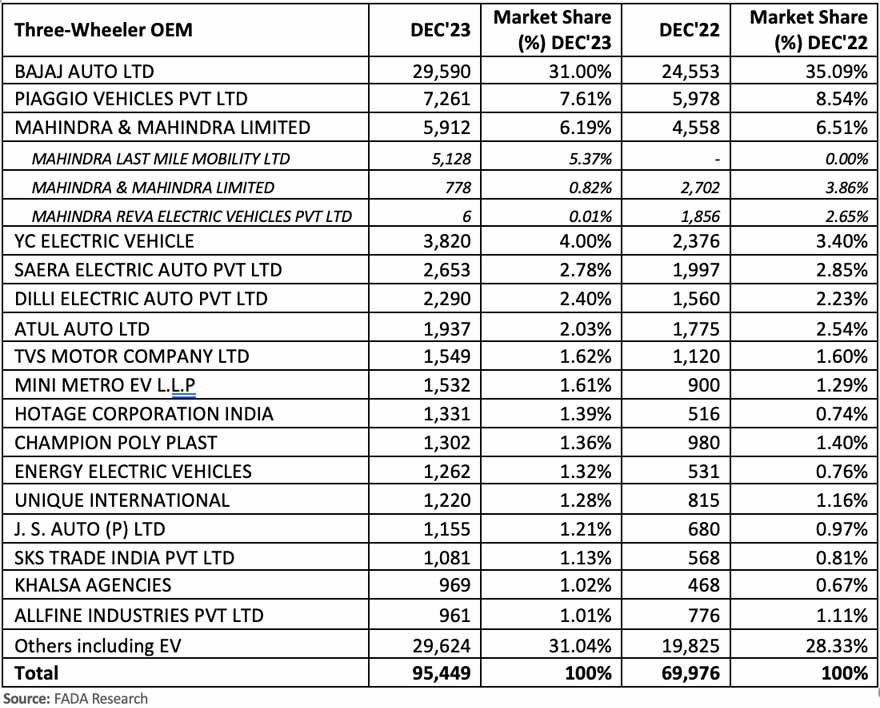

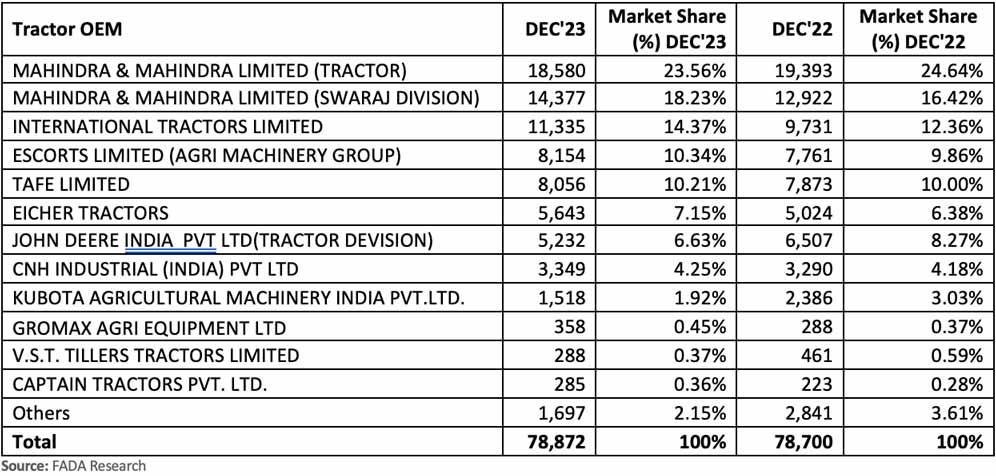

OEM-wise market share data for December 2023 with YoY comparison:

Recommended for you

Leave a Reply

Note: Comments that are unrelated to the post above get automatically filtered into the trash bin.

Leave a Reply

Note: Comments that are unrelated to the post above get automatically filtered into the trash bin.