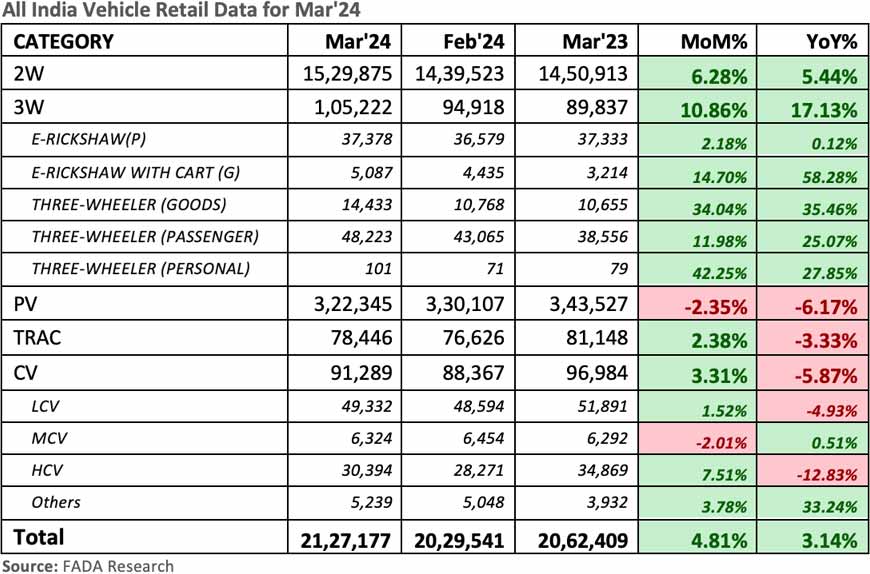

The Federation of Automobile Dealers Associations (FADA) has published March 2024 vehicle retail data, which shows an overall increase of just over 4.8% compared with March 2023 data. The Passenger Vehicle (PV) segment, in particular, sold a total of 3,22,345 units last month, registering a YoY decline of just over 2.3%. Interestingly, in the PV segment, Tata Motors has pushed Hyundai to 3rd place once again while Mahindra and Kia continue to hold their 4th and 5th places, respectively. Toyota continues to hold its 6th place, thanks to the side hustle as a Maruti-Suzuki dealer 😉

Although not a great percentage of growth, all other segments were in green last month. Only the three-wheeler segment has registered a double-digit growth. But anyway, FADA President Manish Raj Singhania had the following to say:

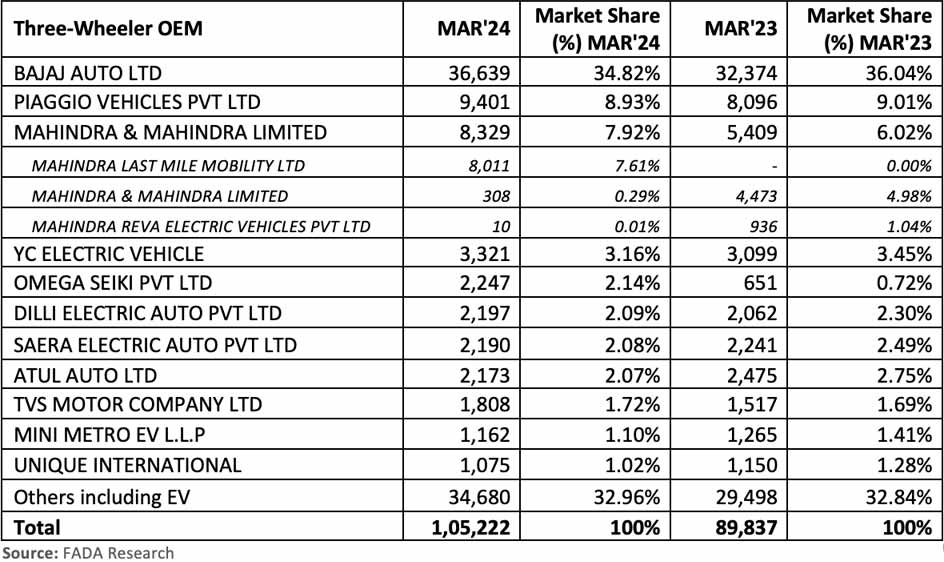

The 2W segment demonstrated resilience and adaptability, with EV sales surging due to the expiration of the FAME 2 subsidy on March 31st. This led to a notable boost in the 2W-EV market share to 9.12%. The 3W segment showed an encouraging sales trend hitting an all-time high retail, driven by the growing acceptance of EVs. The introduction of EV autos and loaders positively impacted the retail environment. Although faced with election-related uncertainties and concerns over policy changes, such as free bus travel for women, the overall outlook for the sector remains upbeat, supported by the quality of vehicles and strong market demand.

The PV sector encountered challenges, with a MoM decrease of over 2% and a YoY fall of over 6%. The downturn was influenced by heavy discounting and selective financing further affected by economic worries and the electoral climate. Nonetheless, positives such as improved vehicle availability, increased stock levels and new model launches did stimulate demand in certain areas. The impact of election activities and changes in festival dates also played a role in sales dynamics.

For the CV sector, March presented a complex scenario. The election announcement resulted in a temporary reduction in purchases, though there is an expectation of a recovery post-election, with decreasing concerns about the forthcoming monsoon. The sector grappled with issues like recent declines, poor agricultural outcomes, discount pressures and financing difficulties. On the upside, there was strong demand in specific areas such as coal and cement transportation, bolstered by bulk orders and vehicle upgrades, which enhanced customer engagement.

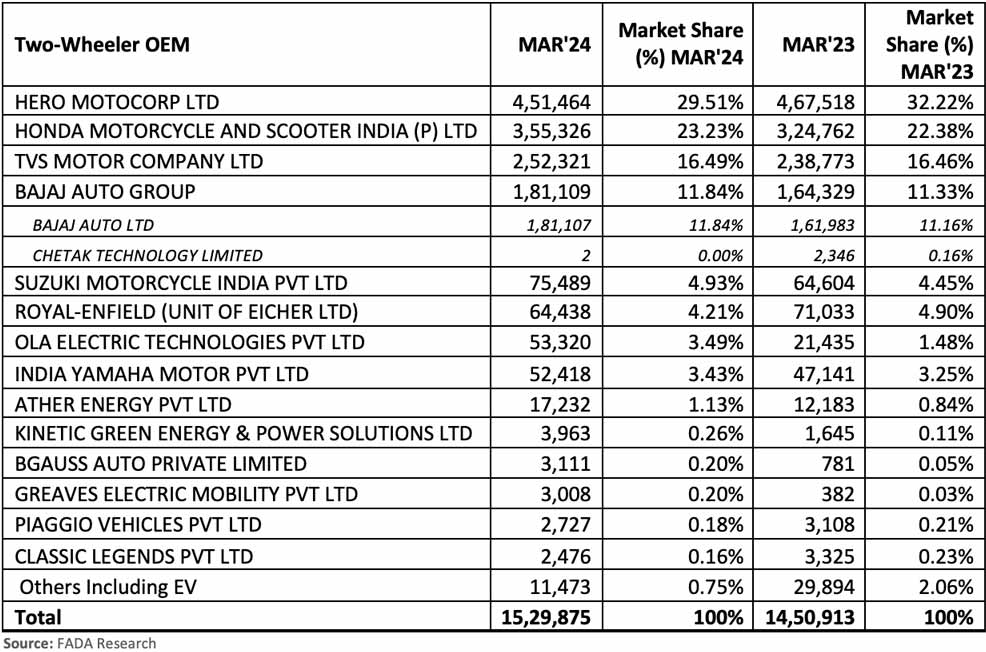

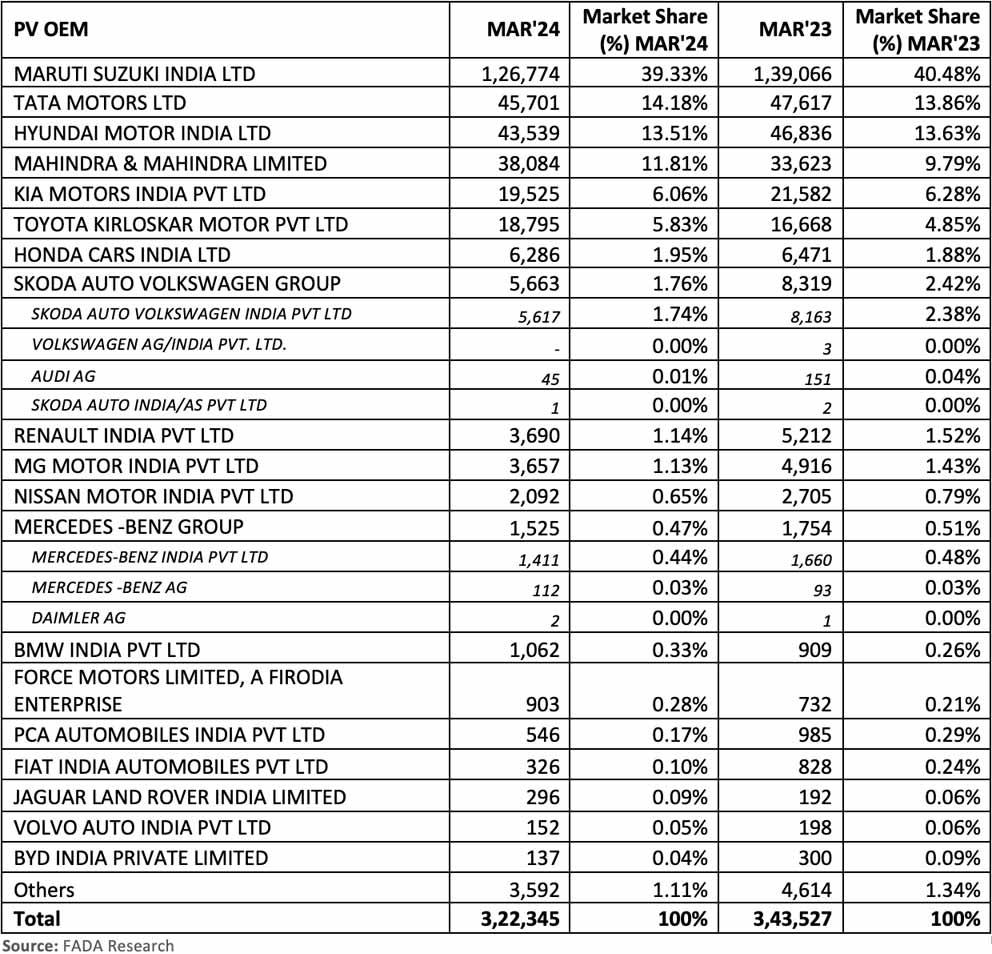

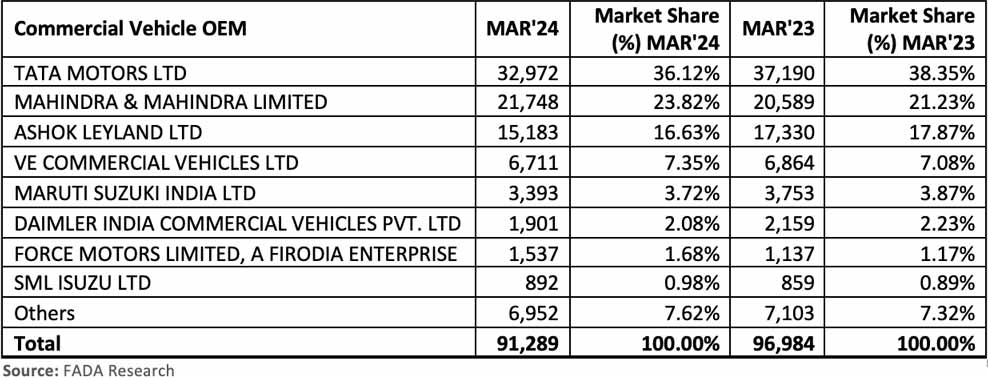

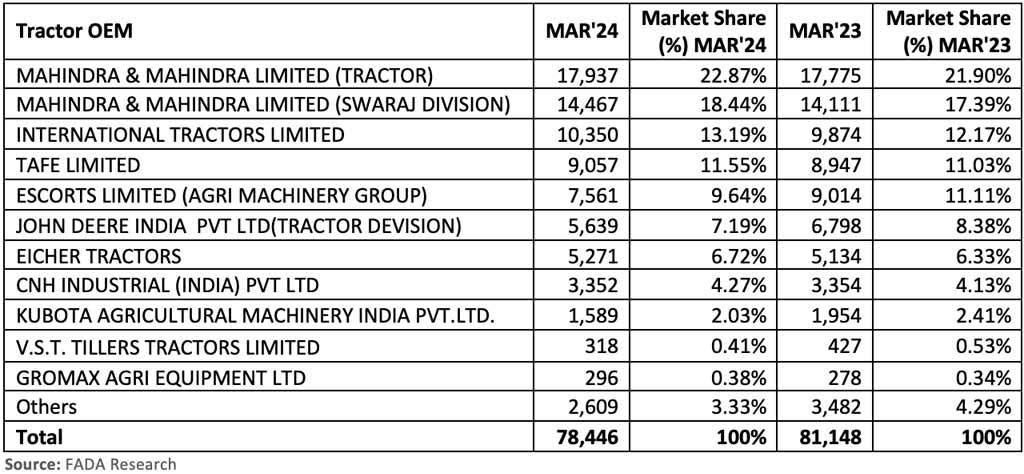

OEM-wise market share data for March 2024 with YoY comparison:

Recommended for you

Leave a Reply

Note: Comments that are unrelated to the post above get automatically filtered into the trash bin.

Leave a Reply

Note: Comments that are unrelated to the post above get automatically filtered into the trash bin.