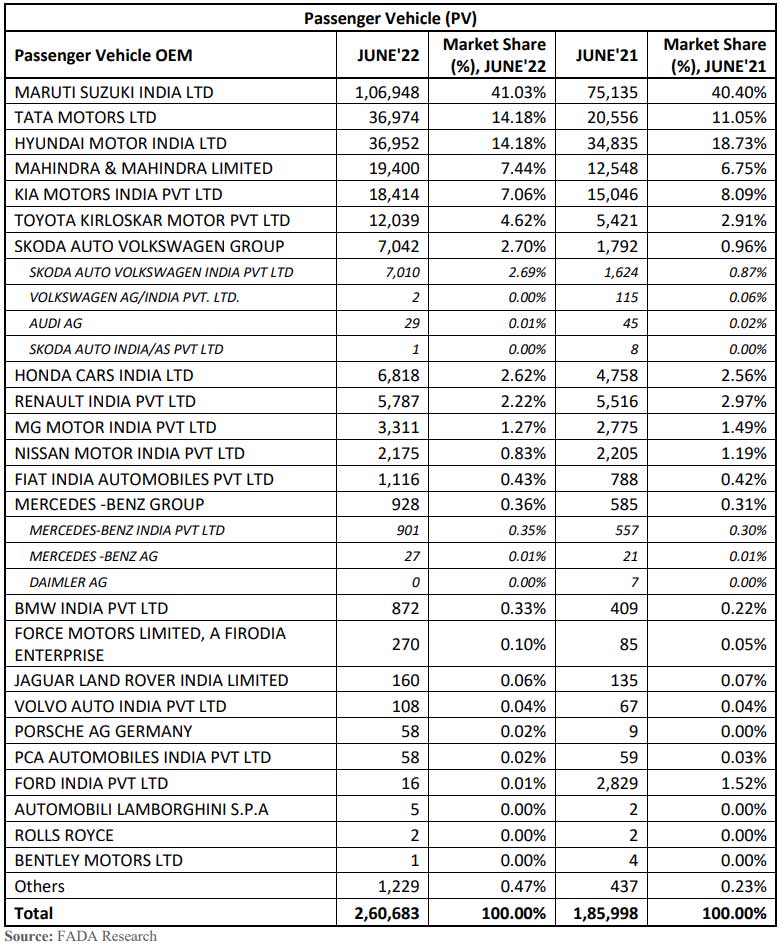

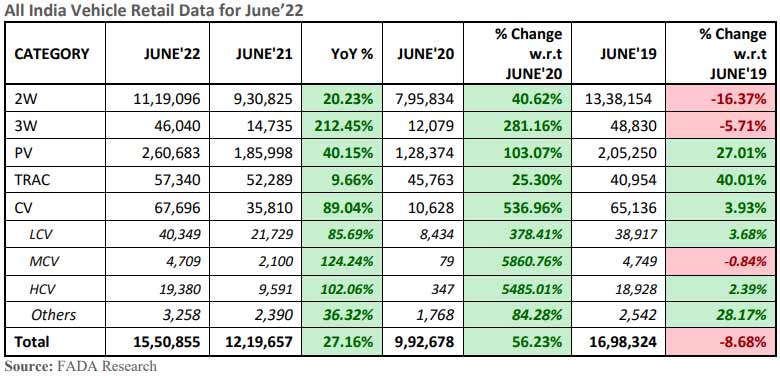

The Federation of Automobile Dealers Associations (FADA) has published June 2022 vehicle retail data, which shows an overall growth of just over 27% compared with June 2021 data. The Passenger Vehicle segment recorded a healthy growth of just over 40% last month. And, Mahindra & Mahindra continues to retain its 4th place by selling 986 more vehicles than Kia, but what’s more interesting is Tata has taken second place this time in the PV segment beating Hyundai by just 22 units.

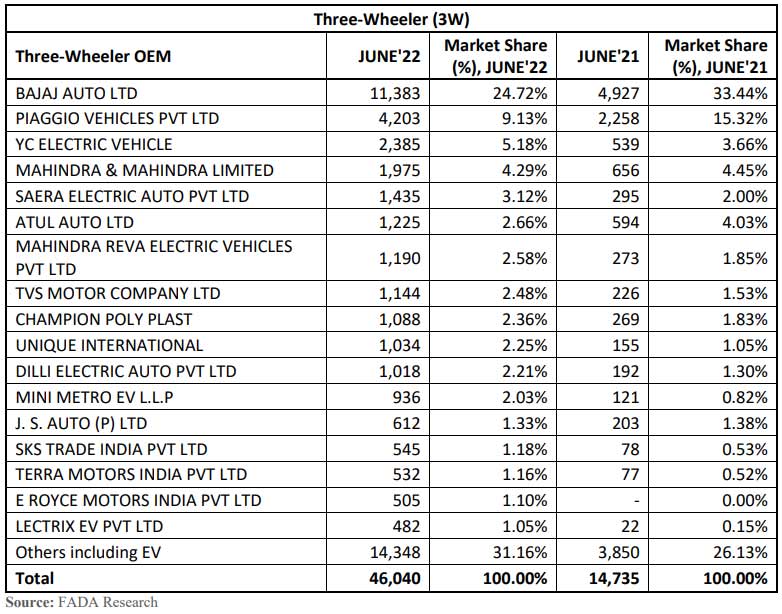

The three-wheeler segment registered a growth of over 212% in June 2022, which according to FADA, is the result of “a major shift” that happened in the electric segment. I guess what FADA is trying to say is that a lot of home delivery companies are operating these electric three-wheelers these days. But anyway, every segment was in green last month. FADA President Vinkesh Gulati had the following to say –

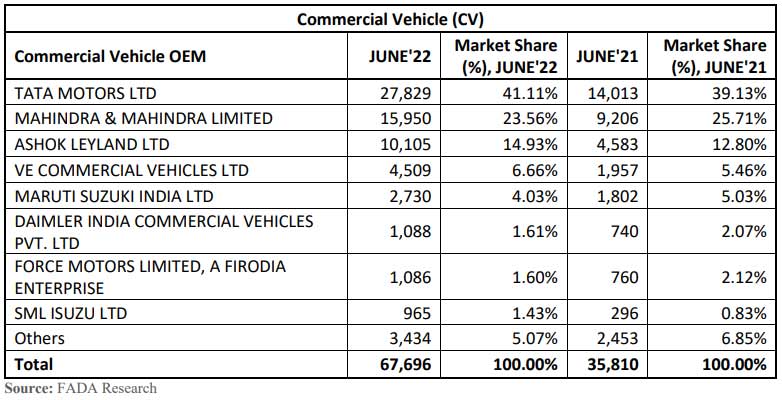

Auto retail for the month of June 2022 continued to show its positive run when compared YoY with June 2021, a month which continued to face the brunt of covid. When compared with June 2019, a pre-covid month, overall sales were down by 9%. Apart from PV and Tractors which were already above the pre-covid level for the last few months and grew by 27% and 40%, CV for the first time showed a growth of 4% thus indicating recovery slowly creeping in for this segment. While 3W narrowed its de-growth and was down by 6%, it’s the 2W segment that still remains the biggest cause of concern and is not picking up as per expectation. The same was down by 16%.

Poor market sentiment especially in rural India, high cost of ownership, inflationary pressure and June generally being a lean month due to rains kept 2W sales at low speed. In the 3W category, a major shift has happened in the electric category. Apart from this, permit issues and frequent price increases remained the biggest dampeners.

The PV segment continued to see robust growth. An increase in wholesale clearly shows that semiconductor availability is now getting easier. Waiting period, especially in compact SUV and mid-size SUV segments continued to remain high. New vehicle launches are seeing robust bookings thus reflecting a healthy demand pipeline. The CV segment showed strength for the first time as it grew by 4% when compared with June 2019, a pre-covid month. Bus segment along with LCVs are showing good traction.

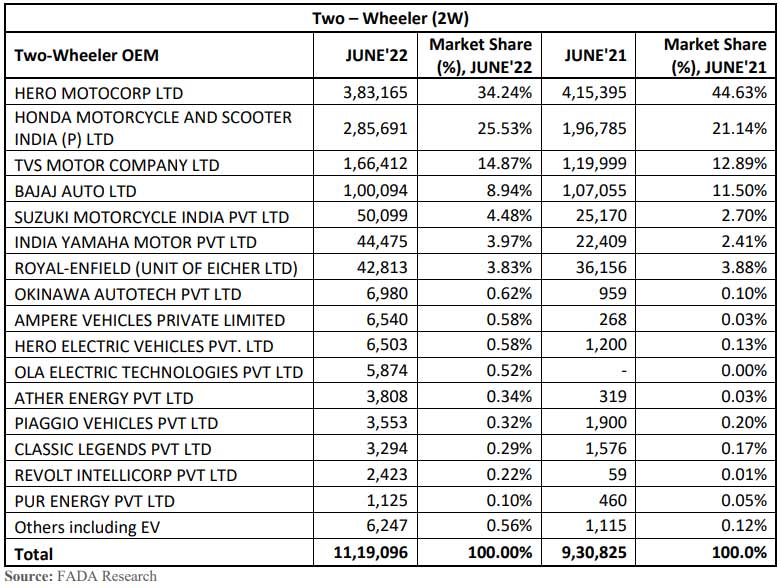

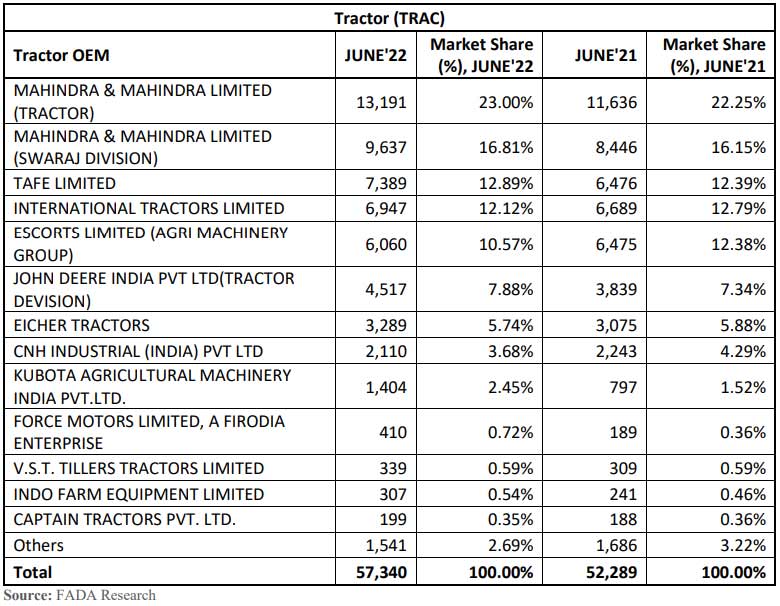

OEM-wise market share data for June 2022 with YoY comparison: