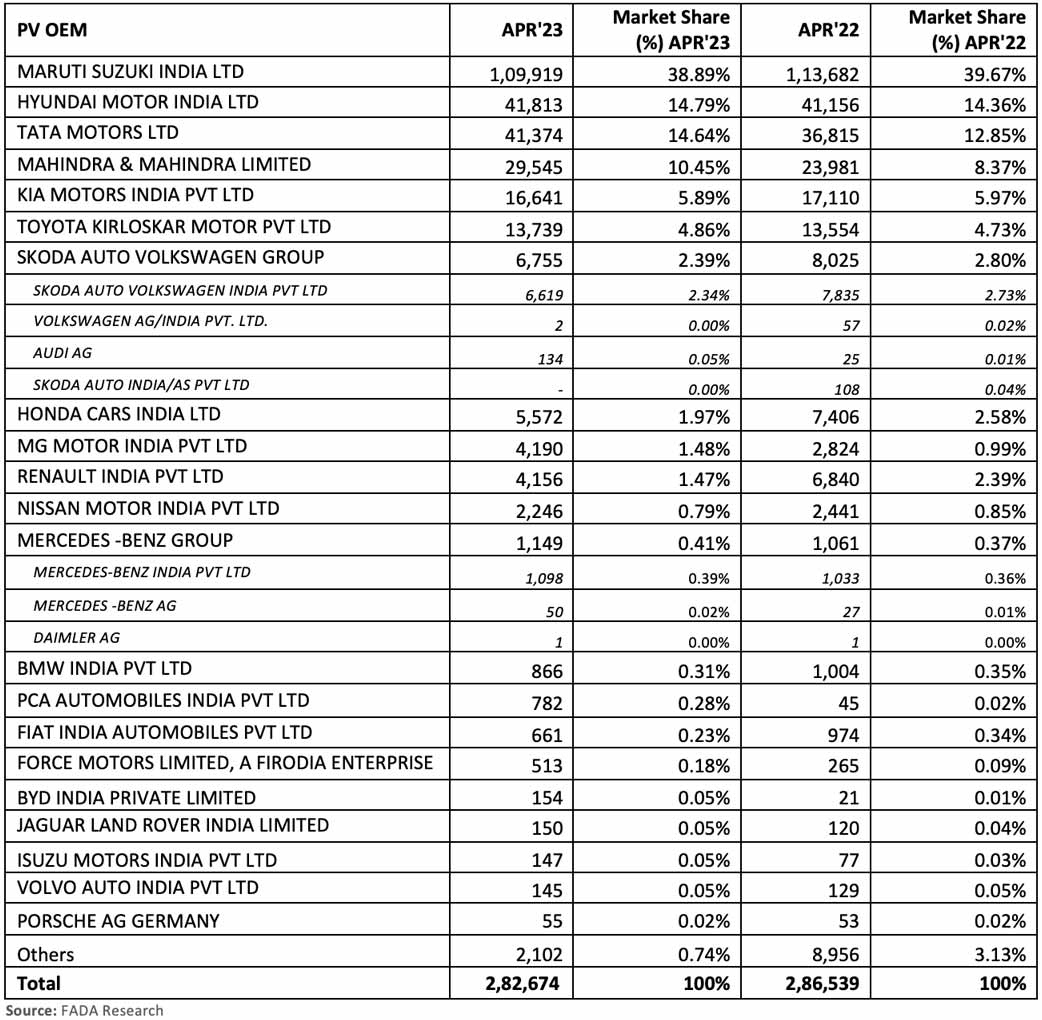

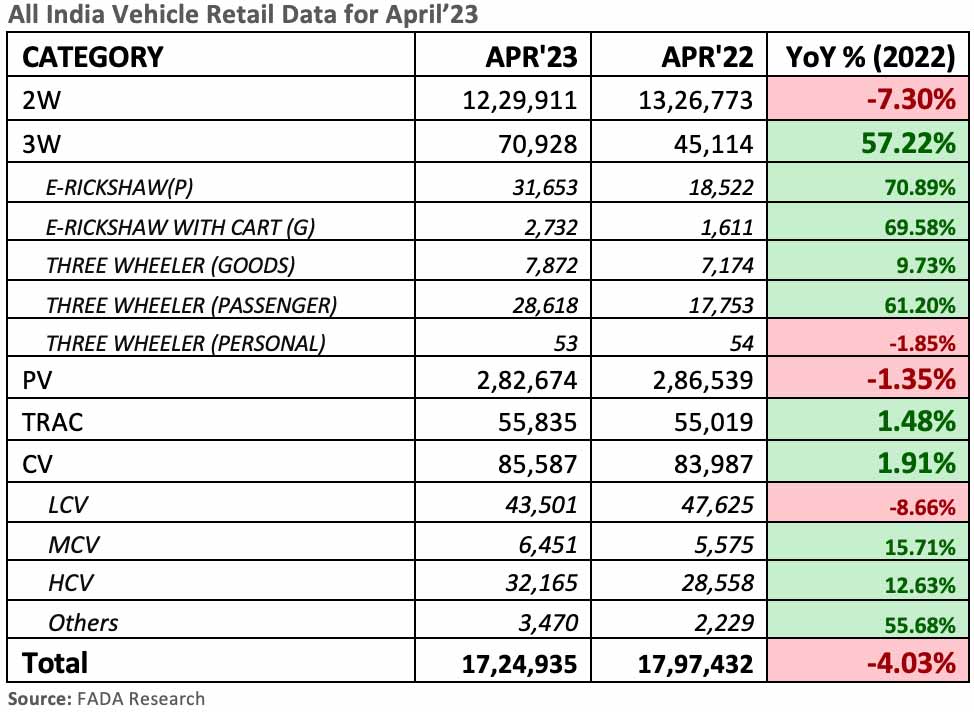

The Federation of Automobile Dealers Associations (FADA) has published April 2023 vehicle retail data, which shows an overall decline of just over 4% compared with April 2022 data. The Passenger Vehicle (PV) segment, in particular, sold a total of 2,82,674 units last month, registering a YoY decline of just over 1.3%. Tata Motors and Mahindra continue to hold their 3rd and 4th place, respectively, in the PV segment. Mahindra dealers retailed over 12,900 PVs more than Kia last month, keeping the latter in 5th place.

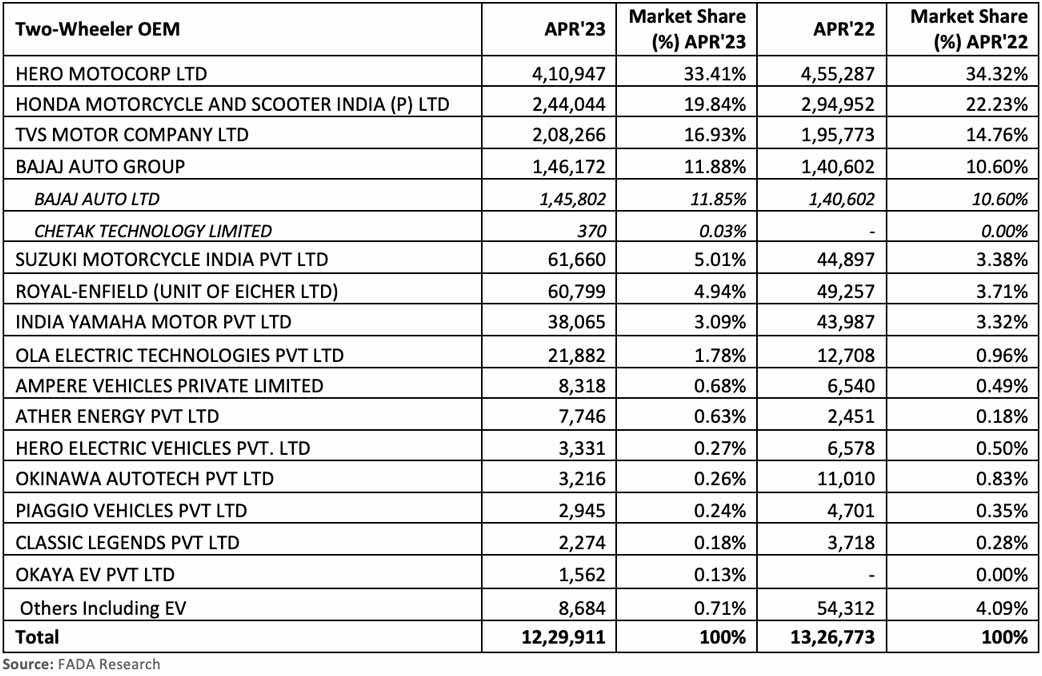

The two-wheeler segment was down by 7.3% last month, while the three-wheeler segment doesn’t seem to show any signs of de-growth. The rest of the segments either show marginal growth or marginal degrowth. FADA President Manish Raj Singhania had the following to say:

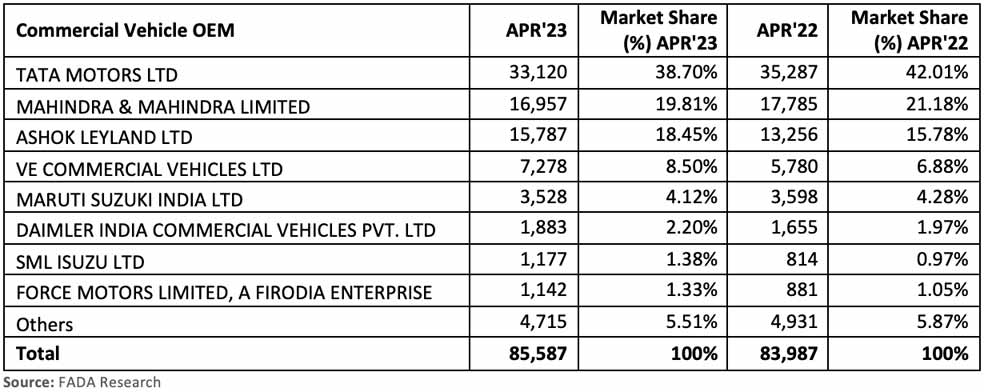

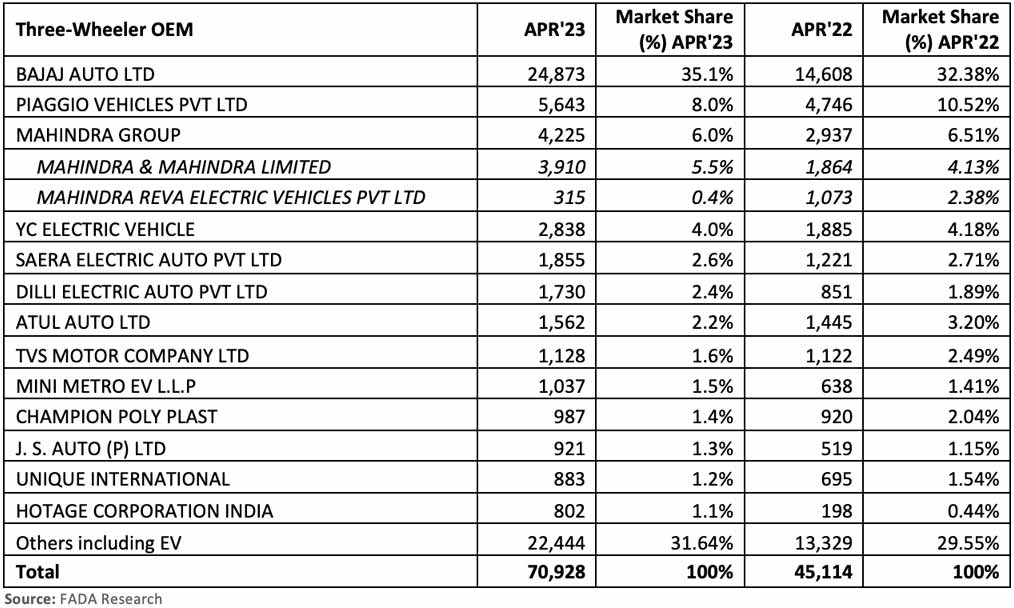

Financial Year 2024 began on a subdued note, with the month of April experiencing a 4% YoY overall decline. Although the three-wheeler segment enjoyed robust growth of 57% YoY, the Tractor and CV segments only grew by a modest 1% and 2%, respectively. Meanwhile, the two-wheeler and Passenger Vehicle segments experienced YoY degrowth of 7% and 1%, respectively.

The two-wheeler segment’s continued low sales, with a 7% YoY decline, can be attributed to limited supplies due to the OBD 2A shift, untimely rains, and pre-buying in March. Model mix availability, rural sentiment, and demand in the motorcycle segment remain weak. The rural economy has yet to show significant progress. Compared to the pre-COVID April 2019, two-wheeler sales are still down by 19%. Thanks to high demand in the e-rickshaw and passenger segments, the three-wheeler segment has grown by 57% YoY and also surpassing pre-COVID levels at a healthy rate.

The Passenger Vehicle segment, which achieved record sales in FY23, slowed down in April, with retail decreasing by 1% YoY. This was primarily due to last year’s high base and the OBD 2A norms, which led to vehicle price increases and advanced purchases in March. Although supplies are improving, there is a significant mismatch between customer demand and available inventory. Furthermore, entry-level PVs have fewer buyers, suggesting that customers at the bottom of the pyramid are still hesitant to upgrade from two-wheelers to four-wheelers. For the first time in 8 months, the PV segment witnessed a YoY degrowth, potentially signaling a tapering demand in this segment.

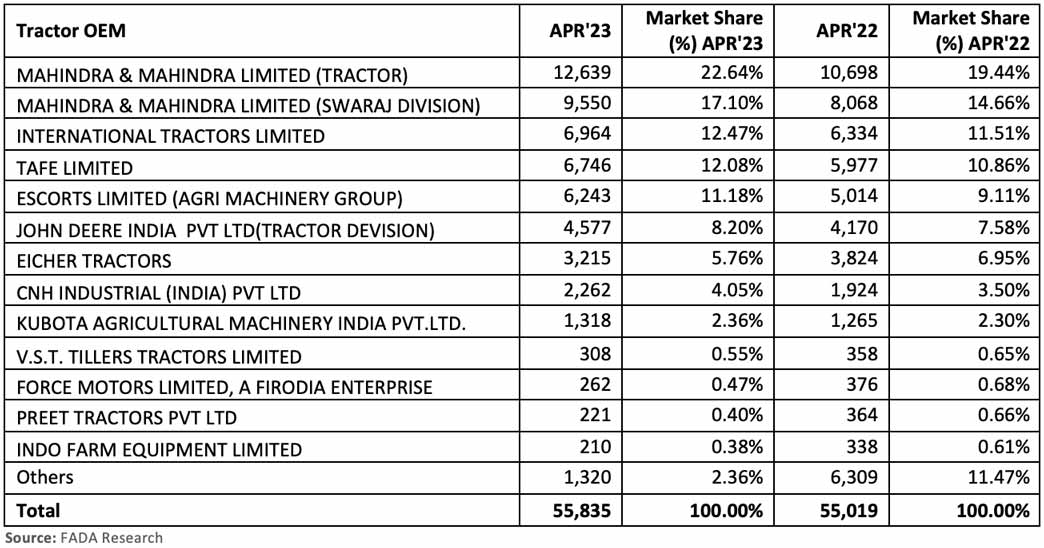

OEM-wise market share data for April 2023 with YoY comparison: